The Value of Geothermal in California

The renewable resource landscape of California is continuously changing due to several factors, notably the state's success in facilitating expansion in renewable energy, which is mostly solar. The state has continued to advance its clean energy policies with the current objective of decarbonization by 2045, an objective guided in part through the California Public Utilities Commission's (CPUC) Integrated Resource Planning (IRP) process and similar planning processes within the large, publicly-owned utilities. Due to these factors, while geothermal is not the lowest cost resource on a levelized cost basis, it is by far the highest economic value in renewable resources that are operating in California and the surrounding region.(1) Even as we see the contract prices for wind, solar PV, and lithium- ion battery prices decline, geothermal's economic value over the life of long-term purchase agreements remains competitive as California and the region move to higher penetrations of renewable energy.

Ormat tracked how solar PV and geothermal energy market values changed over several years. Stand-alone solar energy on the California grid has grown from just under 500 MW in 2010 to over 25 GW of capacity today. This influx has been leading to progressively lower energy market prices during solar production hours and price spikes during the solar ramp periods. Resources, such as geothermal, that can operate outside the solar production hours have maintained a higher market value compared to solar.

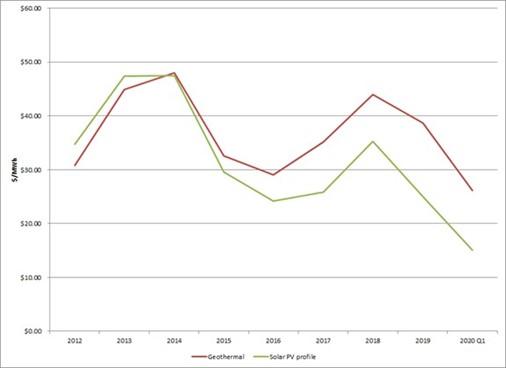

These trends are illustrated in Figure 1 (below) and examine the annual value of a geothermal production profile compared to a sample solar PV production profile taken from a CPUC model from 2012 – 2020 Q1 (January – April).1 At the start of this process, solar energy was worth more than geothermal because it shaved peak energy prices.

However, in the last two to three years, geothermal profiles have been worth around $10/MWh more than a solar profile on average, and commercial forecasts of future energy prices suggest this gap will continue to grow, getting closer to $20/MWh.1 Geothermal's increasing value has persisted into 2020 despite COVID-19 impacts to demand, which decreased solar's value more than geothermal. While the new bulk storage now coming online in California will allow for some energy to be shifted to flatten the “duck curve,” the growing solar energy surpluses will far exceed storage capacity. Hence, forecast models suggest that there will not be much change in this basic pattern for some time.(2)

Another critical factor in the changing value of renewable resources has been the declining RA capacity value of new solar generation. This was predicted in research studies,3 confirmed by the CPUC a few years ago in its RA proceeding, and now its IRP modeling. In California, solar generation has already shaved the annual peak loads and new stand-alone solar no longer provides that benefit. As such, the capacity value of new solar has been adjusted to virtually zero for RA and planning purposes.

Over the past couple of years, this decline in solar capacity value, along with the retirement of older natural gas plants, was reflected in California's bilateral RA capacity prices. These doubled in 2019, reflecting shortages in capacity. This shortage of capacity is why newly-planned solar projects have integrated batteries that enable energy shifting to capture some capacity value. Hybrid resources have not yet proven themselves and are still energy-limited where the storage is charged from the solar field and not the grid.

In contrast, geothermal brings a 90-95% capacity value and a history of reliable operations regardless of the weather. The consistent performance of geothermal as a capacity resource, at all times, is now capturing the attention of buyers across the region.

As the CPUC and California load-serving entities turn to IRPs and other types of long- term analysis to guide procurement and planning decisions, geothermal's multiple values need to be closely examined. California's IRP tools have always selected geothermal at some point in the planning horizon across a range of cost points, even when the model also selects a large amount of solar and storage. The reason geothermal is selected in IRP models is the fact that higher decarbonization targets require the displacement of more and more natural gas-fired and nuclear capacity.

Replacing high-capacity fossil generation in an IRP with renewables results in 1 MW of geothermal displacing 4-5 MW of solar and storage capacity. What we found is that the IRP models build multiple solar plants with storage to displace one geothermal profile. Hence, a simple 1:1 LCOE comparison between these technologies is inadequate. This result is only now starting to be understood by planners; as we look out over the next 20 years, each MW of geothermal procured will require much less solar with storage.

The trends described in this article have been consistent for several years. They suggest that geothermal developers should have confidence that, if more of the resource can be delivered within a reasonable cost range, it will find buyers. A single geothermal project is not competing against the price of a single PV project with storage, but rather the cost of 4 PV projects with storage. It is vital that geothermal developers are helping to tell this story. In addition to stimulating increased geothermal demand across the western United States, these findings should lead to an improved analytical and policy framework for the benefits of geothermal on a global scale.

- Thomsen P. The Increasing Comparative Value of Geothermal in California– Recent Trends and Forecasts as of Mid-2019. Presentation at: Proceedings World Geothermal Congress; April 26 - May 2, 2020;Reykjavik, Iceland.

- All prices used for these calculations are downloaded from the CAISO OASIS website. A table comparing geothermal energy value to three different sample solar profiles used for CPUC modeling can be found in Thomsen (2020, 2018a). This profile is one of the ones in the table, updated to 2020.

- Thomsen P. The Increasing Comparative Value of Geothermal in California–2018 Edition. CD recording: GRC Transactions 2018a;42.